Hard Assets in 2026 — Are You Buying the Right Ones?

I’ve been seeing a lot of noise lately. Gold bar queues at banks or BullionStar. Headlines about Singaporeans dumping AI stocks for gold. Young couples stretching for $2M condos before they get priced out forever. Everyone’s adviser telling them the same thing — volatile times, buy hard assets, protect yourself.

It sounds sensible. But when I actually ran through the options myself, I kept hitting the same wall. Gold doesn’t compound and the crowd has already arrived. Private property ties up a massive cash upfront with years of lock-in — that’s opportunity cost, not protection. Everything else? The advice sounds better than it actually is in practice.

So — what is a hard asset, actually?

Not the textbook definition. The real one.

Something you physically hold or have titled in your name. A gold bar in your safe. Land with a title deed. Not a gold ETF. Not a certificate your bank holds for you. Not a REIT unit. The asset itself — in your hand or legally yours on paper. If your broker goes bust tomorrow, if the bank closes, if the internet goes down — you still have it.

Under that definition the options narrow pretty quickly. And when I looked at each one honestly — price, timing, accessibility — the picture got more complicated than “just buy hard assets” suggests.

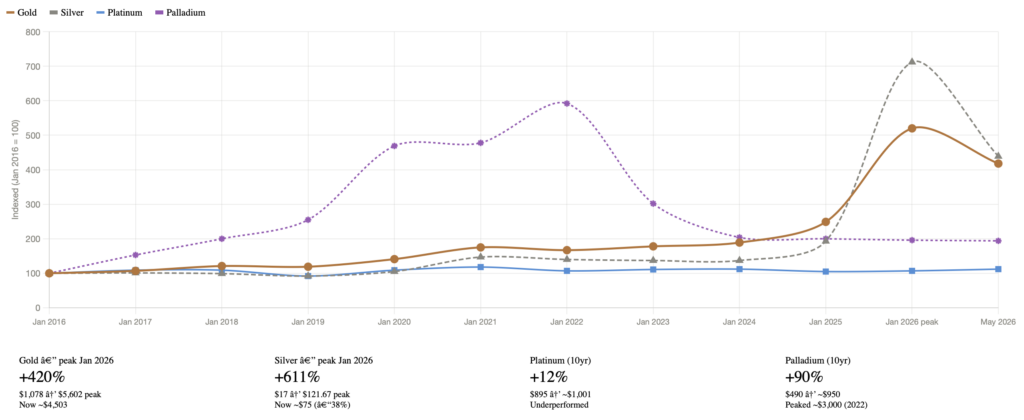

Precious Metals — Gold, Silver, and the Rest

Gold is the obvious first stop. And the case for it is real — scarce, globally recognised, no counterparty risk if you hold the physical bar. I understand why half of Singapore retail investors are now in gold. I was tempted too.

But I looked at the chart above. Gold hit nearly $5,500 an ounce in January — its all-time high per LBMA spot price data. By March it had fallen 15%. The record demand for gold bars in Singapore — the queues at BullionStar, the 100 gram bars flying off the shelf — happened right at the peak. The people who made money on gold bought it in 2023 or 2024, not now.

That’s not a knock on gold as an asset. It’s a knock on the timing. There’s a difference between a good asset and a good entry point. Gold at $2,000 in 2023 was a different bet from gold at $4,600 today after a 64% run in 2025 alone.

The other thing about gold — and this is the part nobody talks about when they’re telling you to buy it — it doesn’t compound. No dividends. No earnings growing underneath it. No business creating value while you sleep. It just sits there. In the long run, stocks win. Gold just preserves. There’s a difference.

Gold is a trade dressed up as an investment. Sometimes it’s the right trade. Right now, after the crowd has already arrived, I’m not sure it is. And if a correction comes — which I think it will — gold is likely to fall with everything else. It’s not the shelter people think it is at this price.

One more thing worth saying clearly: most people buying “gold” in Singapore are not buying a hard asset. A gold savings account at your bank is not gold. A gold certificate is not gold. Those are financial claims on gold — which means there’s a counterparty between you and the metal. If the hard asset argument is about owning something real with no counterparty risk, a bank certificate doesn’t qualify.

Silver tells an even more dramatic story. It hit an all-time high of $121.67 per troy ounce on January 29, 2026 — the highest silver has ever been in nominal dollars, gaining 148% in 2025 alone before the peak. Today it sits around $75. That’s a 38% drop in under four months. The crowd arrived in silver too — just louder and faster than gold.

The case for silver is real and different from gold. It’s more accessible — a 1kg silver bar costs a fraction of a gold bar. And unlike gold, silver has genuine industrial demand layered on top of its monetary role — solar panels, EV components, and grid infrastructure all consume silver at scale. Those fundamentals haven’t changed. But buying silver at $75 after a 611% run from its 2016 base requires the same discipline as buying gold — you need to be clear on whether you’re buying the asset or buying the momentum. Right now, after the run it has had, that distinction matters more than ever.

Platinum and palladium round out the precious metals family — both available in bars and coins, both physically holdable. But they’re more industrial than monetary. Platinum’s fate is tied to hydrogen fuel cell adoption; palladium’s to petrol combustion engines, which are in long-term decline. Interesting in the right context, but harder to position as storm shelters given the structural demand uncertainty.

Property — The Other Obvious Answer

Property is the other obvious answer. And unlike gold, freehold property — known as fee simple ownership in many markets — is genuinely titled in your name. Land. Bricks. Something that exists in the physical world with a legal document saying it belongs to you in perpetuity. Leasehold property, including most apartments, condos, and HDB flats, gives you a titled interest for a fixed term — your name is on the document, but the land reverts when the lease expires. That distinction matters when you’re evaluating property as a hard asset.

While property markets in the US, UK, and Australia have faced corrections or outright slumps over the past two years, Singapore private property prices have been climbing. The market has been defying global gravity — and that divergence has created a particular kind of anxiety. Reports show that younger Singaporeans under 35 are entering the private property market in growing numbers, buying not because they need the space but because they’re afraid they’ll never be able to afford it later. That fear is understandable. But FOMO is not a valuation thesis.

For me, Singapore property doesn’t make sense right now — and it’s not about affordability. It’s about capital allocation. The cash upfront is substantial. Interest rates are elevated and potentially heading higher, not lower. And if a correction comes — which I think is increasingly likely given where bond yields are and what the Fed faces on June 18 — that same capital deployed into quality equities on a dip could generate returns that property at current Singapore prices simply cannot match over the same timeframe.

And the job market is shifting in ways that don’t make the property brochure. This week — Gardenia, H&M, Meta, Standard Chartered all announced job cuts or restructuring in Singapore. AI replacing roles, costs moving to Malaysia. A 25-year mortgage is a 25-year bet on your income. For an under-35 buyer early in their career, that’s worth sitting with before you sign.

Overseas property is the one area where I think there’s genuine value — global markets outside Singapore have corrected meaningfully from their 2022 peaks. In markets like the US where homeownership has become increasingly out of reach for an entire generation, the hard asset conversation looks different again — but the underlying question is the same: what are you actually buying, and at what price? The hidden costs of overseas property are real and they don’t appear in the developer’s brochure. Foreign ownership rules, currency risk, management from a distance, tax treatment across two jurisdictions. Not saying no. Saying go in with your eyes open and proper advice, not a floor plan you fell in love with at a property fair.

Beyond Metals and Property — Watches and the Rest

I’ve been thinking about watches differently lately. Everyone around me is going digital — smartwatches, phone payments, everything on a screen. And yet the secondary market for a good Rolex or Patek keeps holding up. Which made me ask — does an analog mechanical watch still have a future as a store of value in a digital world?

My honest answer: a Patek Philippe was never really competing with a smartwatch to begin with. It’s not about telling the time. It’s about craftsmanship, legacy, and scarcity in a world drowning in mass-produced digital everything. If anything, that scarcity story may get stronger, not weaker. The question is whether the next generation of buyers feels the same way — and that’s not something the data can tell you.

What the data can tell you is how specific models have actually performed. If you want to do your research before walking into a dealer, WatchCharts tracks secondary market prices by model — you can look up any reference and see exactly where prices have been.

Here’s what the numbers look like across timeframes (source: WatchCharts, May 21 2026):

| Model | 3-month | 6-month | 1-year | 2-year |

|---|---|---|---|---|

| Overall Market Index | +1.4% | +5.0% | +9.1% | +5.1% |

| Patek Philippe 5711/1A | –1.1% | +2.4% | +25.5% | +25.4% |

| Rolex Sky-Dweller | +0.6% | +1.5% | +4.7% | –2.0% |

| AP Royal Oak 26470ST | –3.7% | –5.0% | –3.7% | –3.4% |

| IWC 387901 | –4.3% | –6.1% | –12.7% | –12.7% |

Fine wine and art deserve a mention too — both physically held, genuinely scarce. Fine wine prices are near five-year lows heading into 2026, which looks interesting on paper. But Gen Z drinks significantly less than previous generations — the long-term demand thesis is worth questioning before you commit capital. Art requires deep expertise, high transaction costs, and authentication knowledge most retail investors don’t have. I don’t hold either — not because they don’t work, but because they require expertise I don’t have.

So Where Does That Leave Us?

I’ll be honest — when I ran through every option, nothing felt like a clean answer. Gold had already run. Private property in Singapore is priced like nothing can go wrong — and that’s exactly when I get nervous. Overseas property is interesting but complicated. Watches and wine require expertise and patience I may not have. Every supposed safe harbour has a catch in 2026.

And the environment isn’t making it easier to think clearly. Bond yields are at their highest since 2007 — the kind of level that historically precedes something breaking. The DBS CEO just sold S$6 million of her own shares (SGX: D05) after the stock hit S$60. When the people closest to the market are quietly stepping back, that tells you something.

And beneath the headlines, US credit card debt has hit $1.25 trillion — serious delinquencies at 13.1%, the highest in 15 years, with more than 1 in 10 borrowers making only minimum payments at 21% interest rates. The people rushing into hard assets aren’t doing it from a position of strength. They’re doing it from fear. That’s a different kind of buying, and it tends to end badly.

What I actually did was less exciting than buying gold bars or signing on the dotted line for a property. I trimmed the volatile positions. I passed on gold at the peak. I passed on Singapore private property. I’m watching overseas markets. And on the watch front — I know exactly which references I’d want and what I’d pay before I walked into any dealer.

The cash I’ve freed up isn’t sitting idle though. Holding cash has its own cost — inflation in the US is running at 3.8%, 3.2% across Southeast Asia, 1.2% in China, and 1–2% here in Singapore. Every month in a savings account is purchasing power quietly slipping away. So I’m parked in short-duration instruments — T-bills, money market funds — that at least partially fight back while I wait for the right entry point.

The advisers aren’t wrong that the macro environment supports owning real things. But buying gold, buying property — that advice assumes you’re getting in at the right price, at the right time, in the right form. Most people rushing into BullionStar right now aren’t doing that calculation. They’re responding to fear.

Could I be wrong? Yes. If the correction never comes and markets keep running, this is opportunity cost. I’m aware of that. But I’d rather miss some upside than buy the wrong thing at the wrong price because I felt pressured to act. That’s a decision I can live with. The question is whether you can live with yours.

This article represents my personal opinion and investment decisions. It is not financial advice or investment research. Always do your own research and consult a qualified financial advisor before making any investment decisions.