The Central Provident Fund (CPF) is a comprehensive social security system in Singapore designed to provide financial security and retirement savings for its citizens. Among the various CPF accounts, the CPF Ordinary Account (OA) holds contributions for housing, education, investment, and healthcare expenses. While the CPF OA offers a competitive interest rate, you may consider exploring alternative investment opportunities to potentially maximize your returns. I would like to discuss the benefits and considerations of investing CPF OA funds to align with F.I.R.E. goals and achieve long-term financial growth.

Understanding CPF Ordinary Account (CPFOA) Returns:

By default, CPF OA funds earn an interest rate, reviewed quarterly and benchmarked against the 12-month average yield of 10-year Singapore Government Securities (10YSGS) plus an additional 1%. As of today, the interest rate for the OA is 2.5% compounded per annum. While this rate is higher than many traditional savings accounts, some individuals may seek higher returns by exploring other investment avenues.

Tax Implications on CPFOA Returns

One important consideration when investing CPF Ordinary Account (CPFOA) funds is the tax implications on the returns generated. Generally, the returns earned from CPFOA investments are not subject to income tax. This means that any interest, dividends, or capital gains obtained through investments made using CPFOA funds are exempt from taxation. Great to know! – This tax advantage can be beneficial for individuals seeking to maximize their investment returns and achieve long-term financial growth. However, it is important to note that tax regulations may change over time, and it is advisable to stay updated with the latest tax policies and consult with a qualified tax professional to ensure compliance with tax obligations.

Investment Options for CPF OA Funds tablulated below:

- Shares

When it comes to investing directly in equities, one of the key benefits is the potential for higher returns. By selecting individual stocks, I also enjoy having the opportunity to capitalize on the growth of specific companies or sectors. Direct investing also allows for greater control and customization of my portfolio, as I can handpick stocks that align with my investment goals and risk tolerance. However, direct equity investment requires a significant amount of research, time, and expertise to identify suitable stocks and manage a diversified portfolio effectively. It also exposes investors, including myself, to individual stock risks and market volatility, making it a riskier approach for inexperienced investors. Therefore, when considering investing my CPFOA funds directly in equities, my objective is to strive for a minimum Net Internal Rate of Return (Net IRR) of 8% or, in the worst-case scenario, achieve a Net IRR of 3%.

- UTs, ILPs, ETFs, Managed Funds, etc

Investing in mutual funds or managed funds, offers several advantages. These funds provide diversification by pooling money from various investors to create a portfolio of different securities. This diversification helps spread risk and reduces the impact of individual stock fluctuations. These funds are managed by professional fund managers who have expertise in selecting and managing a diversified portfolio, relieving individual investors from the burden of extensive research and monitoring. Additionally, these provide accessibility, allowing investors with smaller capital to gain exposure to a wide range of stocks. However, these funds often come with management fees and other expenses, which can eat into the overall returns. Investors also have limited control over the specific stocks included in the fund, and the performance of the unit trust depends on the decisions made by the fund manager. Generally, I’m not an advocate and personally believe that the net returns may likely be low and may not be able to achieve a Net IRR of 3% in a worst case scenario. Hence, it might be better to leave the CPFOA monies in the OA account for the long run.

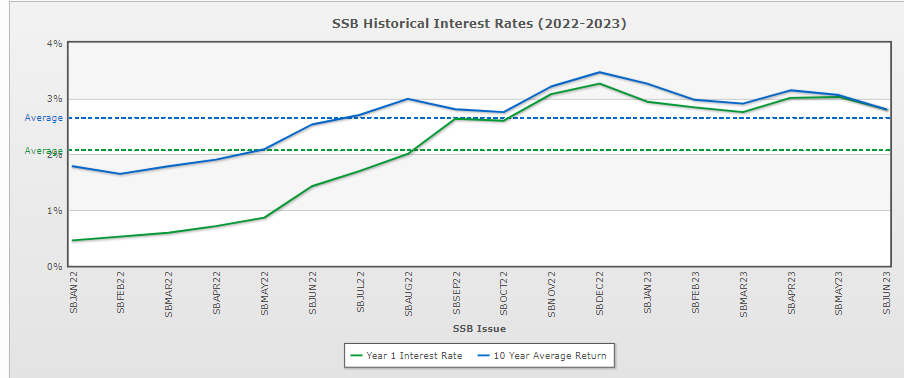

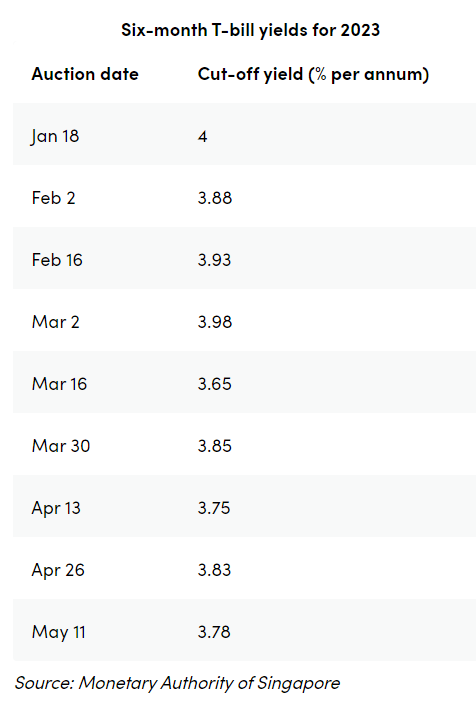

- FDs, SSBs, Treasury Bills, etc

In recent times, there has been a significant development in the financial landscape with regards to interest rates. Central banks and monetary authorities have implemented interest rate hikes to address changing economic conditions and inflationary pressures. As such, many investors are flocking to Banks’ fixed deposits as well as the Singapore Savings Bonds and Treasury Bills, which are guaranteed by the Singapore Government.

As there are sudden huge demand for these products, the amount you can invest is likely limited, for example:

- Buying SSBs/T-Bills Auction Process – In recent auctions, I managed to only secure an allocation of between SGD10,000 to SGD50,000, which I was hoping for a higher amount.

- Placing CPFOA Fixed Deposit – I was at several local banks yesterday and the only bank that offers CPFOA fixed deposits is OCBC at the rate of 3.2% and for a short period of 6 months. They also imposed a deposit limit of SGD99,999 per customer which was disappointing.

- Placing Cash Fixed Deposit – Similarly, I was surprised to learn that several of the local banks have also imposed a deposit limit of SGD99,999 per customer.

While the CPF Ordinary Account (CPFOA) provides a secure means of saving for various expenses, exploring alternative investment options can potentially enhance long-term financial growth for those pursuing FIRE. By comprehending the investment landscape and carefully evaluating individual financial goals, risk tolerance, and knowledge of investment options, individuals can make informed decisions to optimize their CPF OA funds for achieving FIRE objectives. By harnessing the potential of CPFIS, SSBs, and real estate investments, you can diversify your portfolios and potentially earn higher returns. However, it is crucial to consider factors such as time horizon, risk management, diversification, and liquidity when making investment choices. By strategizing and leveraging the investment potential of CPFOA, you can take significant steps towards achieving FIRE and attaining long-term financial growth and independence.

Credits to:

- Central Provident Fund (CPF) – CPFB | CPF Investment Scheme (CPFIS)

- Monetary Authority of Singapore (MAS) – Bonds & Bills (mas.gov.sg)

- Channelnewsasia – Investors still hot on less risky bets. But with waning returns, is it time to move on? (channelnewsasia.com)

Disclaimer: The information provided on this blog is for general informational purposes only. All information on the blog is provided in good faith, however we make no representation or warranty of any kind, express or implied, regarding the accuracy, adequacy, validity, reliability, availability, or completeness of any information on the blog. Under no circumstance shall we have any liability to you for any loss or damage of any kind incurred as a result of the use of the blog or reliance on any information provided on the blog. Your use of the blog and your reliance on any information on the blog is solely at your own risk.

Please note that the information and opinions expressed on this blog are solely those of the author(s) and do not necessarily reflect the views or opinions of any organization, employer, or affiliated individuals. The content on this blog is not intended to be a substitute for professional advice, diagnosis, or treatment. Always seek the advice of your physician, lawyer, or other qualified professional with any questions you may have regarding a specific situation.

We reserve the right to make additions, deletions, or modifications to the content on this blog at any time without prior notice. We do not guarantee that the blog will be available at all times or that the content on the blog will be free from errors or omissions.