As the cost of living in Singapore continues to rise due to inflation, many families are considering a move to Johor Bahru while commuting to Singapore for work, and their children attend international schools. The allure of seemingly cheaper properties across the causeway and in other countries is enticing, but it’s crucial to examine whether they are genuinely affordable. Moreover, there have been numerous stories of global investors incurring losses on Malaysian properties in projects like Iskandar and Country Garden’s Forest City. Therefore, it’s essential to consider local affordability as part of your exit strategy when purchasing a property abroad. In this blog, we will explore the crucial factors impacting affordability, including median household incomes, and provide examples to guide your approach when buying an overseas property, focusing on Malaysia.

- Researching the Real Estate Market

Conducting thorough research on the real estate market in the target country is crucial before making any investment decisions. Study local property trends, market conditions, and factors influencing property prices such as economic stability, population growth, and government policies.

If you’re a Singaporean citizen and own an HDB flat, you will need to meet your Minimum Occupation Period (MOP) before you can buy property in Malaysia.

Most property and land types are fair game, but you won’t be able to purchase the following as a foreigner:

- Bumi lots (Land reserved for Bumiputeras)

- Agricultural land (Exceptions can be made if the land is over 5 acres and will be used for commercial purposes)

- Malay reserved land (Land that can only be sold exclusively to Malays)

- Property with a valuation below RM 1 million

Foreigners may consider buying Malaysian properties under the Malaysia My 2nd Home (MM2H) visa, which makes property ownership more affordable for the long-term.

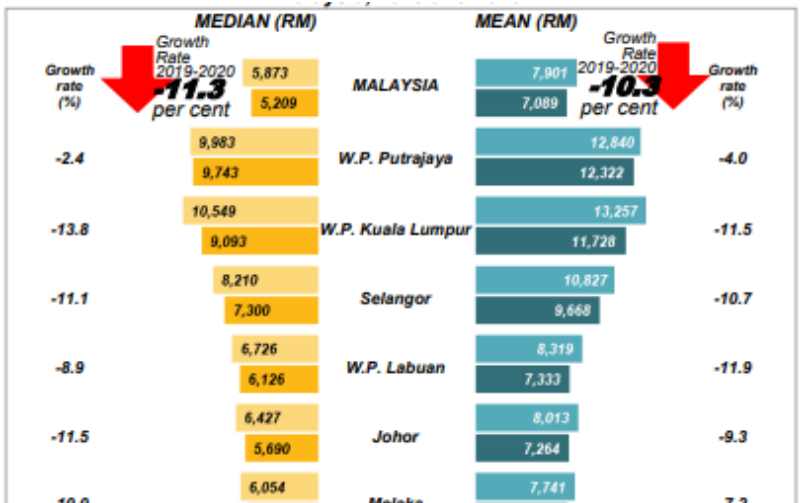

- Median Household Disposable Income in Malaysia

Understanding the median salaries of locals in Malaysia is essential to determine if property prices align with their earning capacity.

As of 2020, the median household income in Malaysia was around MYR 5,209 per month (approximately SGD 1,520). Please note that updated data from the Malaysian Government is expected to be released soon.

- Applying the Mortgage Servicing Ratio (MSR) and Total debt servicing ratio (TDSR)

The Mortgage Servicing Ratio (MSR) is a critical factor in evaluating local affordability. It represents the proportion of a borrower’s gross monthly income that can be used to service their mortgage loan.

In Singapore, the MSR is capped at 30% of a borrower’s gross monthly income, while the borrower’s Total Debt Servicing Ratio (TDSR) should be less than or equal to 55%. These ratios provide guidelines for determining an individual’s ability to manage their debt obligations.

To illustrate the concept, we will use the same assumptions for each property example.

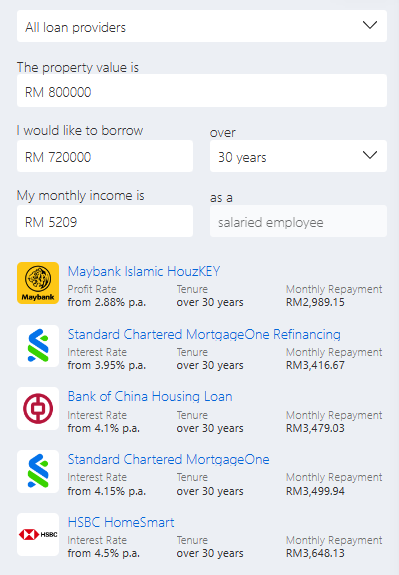

Property 1: A Singaporean/foreign family of three purchasing a 720 sqft, three-bedroom unit at The Coronade Residences, with an expected completion in 2025. The selling price is RM 800,000 (approximately SGD 233,600), partially furnished.

While the price may seem inexpensive from a Singaporean perspective, let’s analyze whether it aligns with the earning capacity of locals and if it would be easy to sell in the future.

The median monthly household income in Malaysia is RM 5,209. Based on the MSR capped at 30%, a typical Malaysian household can allocate up to RM 1,563 towards mortgage payments. Assuming a loan amount of RM 720,100 (90% financing) for 30 years, the estimated monthly mortgage payments range between RM 2,989 and RM 3,648, using rates provided by RinggitPlus.

Considering the local median income and affordability, this condominium may be relatively unaffordable for a typical Malaysian household, especially for those seeking larger units. For comparison, a search on PropertyGuruMY reveals a 999 sqft, three-bedroom condominium located 8 minutes from CIQ, Johor, renting for RM 2,000.

It’s important to note that Singaporean or foreign buyers may face challenges selling the property in the future due to limited local demand at inflated prices.

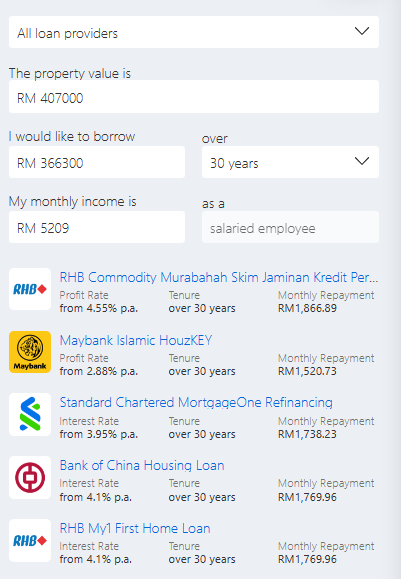

Example 2: A Singaporean/foreign retired couple buying a 1,001 sqft, three-bedroom unit at D’starlingtton, with an expected completion in 2026. The purchase price is RM 407,000 (approximately SGD 119,000), unfurnished.

Similarly, let’s analyze whether this purchase aligns with the earning capacity of locals.

With the median monthly household income in Malaysia at RM 5,209, the MSR capped at 30%, and assuming a loan amount of RM 366,300 (90% financing) for 30 years, the estimated monthly mortgage payments range between RM 1,520 and RM 1,867, using rates provided by RinggitPlus.

A search on PropertyGuruMY reveals a nearby, 1,000 sqft, three-bedroom condominium renting for RM 1,600.

Considering the median income and rental prices, this property seems relatively affordable for a typical Malaysian household. Retirees may choose between renting and buying, with property ownership potentially driven by legacy reasons.

- Legal and Tax Implications

Each country has its unique legal and tax requirements for foreign property buyers. Engage with local legal experts to understand the buying process, tax implications, and potential additional costs involved.

- Cost of Living and Lifestyle Considerations

Take into account the cost of living in the area where the property is located, as it may vary significantly from what you’re accustomed to in Singapore. Additionally, consider lifestyle preferences, proximity to amenities, and accessibility to transportation networks.

Conclusion

Considering local affordability is crucial for both Singaporean/foreign buyers and the residents of the target country when purchasing a property abroad. By analyzing median househould incomes alongside property prices, we can determine if owning a certain property in Malaysia aligns with the earning capacity of locals. Thorough research on the real estate market, exchange rates, legal implications, cost of living, and lifestyle preferences will contribute to making an informed decision when investing in overseas property.

Other Information references:

- RinggitPlus Home Loan – Best Housing Loans in Malaysia 2023 – Compare and Apply Online (ringgitplus.com)

- PropertyGuruMY – Search Property and Real Estate for Sale, for Rent in Malaysia | PropertyGuru Malaysia

- Department of Statistics Malaysia – Department of Statistics Malaysia (dosm.gov.my)

Disclaimer: The information provided on this platform is for general informational purposes only and does not constitute professional advice. While we strive to keep the information up-to-date and accurate, we make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability concerning the content provided. Any reliance you place on the information is strictly at your own risk. We shall not be liable for any losses or damages, including without limitation, indirect or consequential loss or damage, arising from the use of this platform. Always seek the advice of a qualified professional or expert for specific advice related to your circumstances.